· Views 8,424

Market Review:

The Fed held its rate steady at 3.50%-3.75% on Wednesday, June 17, just as expected. But everything else about Kevin Warsh's first meeting as chairman was a surprise: a much shorter policy statement, a more hawkish outlook, and a press conference that rattled traders. Stocks fell, yields rose, the dollar surged, and gold dropped. What was supposed to be a quiet meeting turned into one of the biggest Fed days in recent memory.

A Statement Half the Length, and a Key Phrase Missing

The vote itself was unanimous, 12-0, a notable contrast to the four dissents recorded at the final meeting under former Chair Jerome Powell back in April. Yet the unity masked a meaningful shift underneath. The post-meeting statement ran just 130 words, compared with 341 words in April's release. Warsh had promised "regime change" at the Fed, and the first visible evidence of it was an announcement stripped down to bare essentials: solid economic activity, strong productivity and investment, a labor market holding steady, and inflation still running hot, in part because of energy-related supply shocks tied to the Middle East conflict. The line that grabbed traders' attention, however, was what got cut. Language that had previously hinted at "additional rate adjustments," widely read as a signal the Fed's next move would be a cut, was removed entirely. In its place there was a single, blunt declaration: the Committee will deliver price stability. No mention of the Fed's other mandate, full employment, made it into the final text at all.

The Dot Plot Flips From Cuts to Hikes

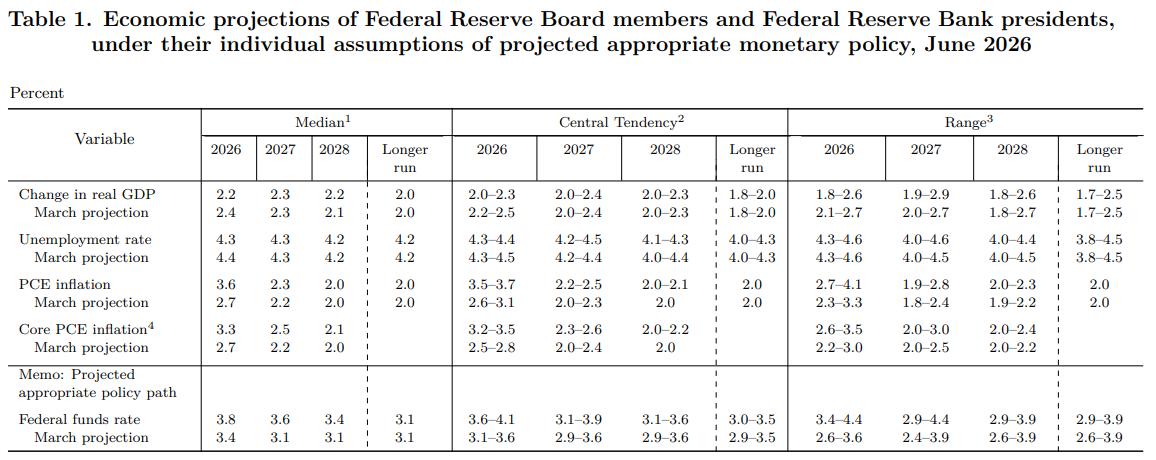

If the statement was restrained, the quarterly Summary of Economic Projections was anything but. Back in March, not a single policymaker penciled in a rate hike for 2026, and the committee's collective view pointed to one rate cut by year-end. In June, that picture reversed. Nine of the eighteen participants who submitted projections said they could support at least one hike before the year is out, six of those for two separate quarter-point increases, while eight preferred holding steady and just one still saw room for a cut. The median dot for the federal funds rate at the end of 2026 moved up to 3.8%, above the current 3.625% midpoint, effectively signaling that the committee's base case has shifted from easing to a possible tightening.

Inflation forecasts told the same story. Headline PCE inflation for 2026 was revised up to a median of 3.6%, nearly a full percentage point above the 2.7% the Fed projected back in March. Core PCE jumped to 3.3% from 2.7%. Growth forecasts moved modestly lower, with 2026 GDP now seen at 2.2% versus 2.4% previously, while the unemployment rate outlook ticked down slightly to 4.3%. Taken together, the projections describe an economy still expanding but facing inflation that policymakers no longer expect to fade quickly on their own.

One detail made headlines on its own: Warsh chose not to submit a personal dot at all, the only one of the nineteen participants to abstain. He has long argued that the dot plot can box the Fed into defending positions publicly before the data warrants it, and at his press conference he said simply that the projections aren't something he finds useful for himself, even as he encouraged colleagues to keep submitting theirs.

Warsh's Press Conference: Reform Comes Before Easing

If there was any doubt about where the new chairman's priorities sit, his first news conference erased it. Warsh leaned repeatedly on the idea that the Fed's commitment to price stability is "strong, unanimous, and unambiguous," and said bluntly that persistently high prices have been a burden on ordinary households for five years that the Fed allowed to go unaddressed. He was equally direct that the 2% inflation target itself wasn't up for debate, telling reporters it remains the Fed's long-held objective and won't be revisited until it's actually been hit.

Beyond the inflation message, Warsh used the platform to announce a structural shake-up: five new task forces that will examine the Fed's communications, its balance sheet, the data it relies on, productivity and the impact of artificial intelligence on the economy, and the framework behind its inflation approach. He was careful to frame this as deliberation rather than outsourcing, noting the task forces would produce recommendations the committee could accept, reject, or argue over, not policy made by committee staff. Several Wall Street voices read the overall tone as more hawkish than expected. BlackRock's Rick Rieder called it the start of a new era in the U.S. monetary policy, while Evercore ISI's Krishna Guha noted that the chairman sounded like the inflation hawk Warsh was known as during his earlier stint as a Fed governor. DoubleLine's Jeffrey Gundlach was blunter still, saying the easy-money chairman many investors expected when Warsh was nominated simply didn't show up.

How Markets Reacted

The reaction across asset classes was immediate and largely one-directional. Equities slid through the afternoon of June 17, with the S&P 500 closing down around 1.2%, the Nasdaq Composite off roughly 1.3%, and the Dow shedding more than 500 points. Treasury yields jumped as traders repriced the odds of a hike, with the two-year yield climbing as much as 16 basis points to its highest level in over a year, while the ten-year added a more modest four basis points. The dollar index rallied close to 1%, its strongest single-day gain in nearly a year, reflecting the market's quick pivot toward expecting higher-for-longer rates. Gold, which tends to struggle when real yields and the dollar rises together, fell more than 2% and slipped back toward $4,260 area after trading above $4,300 earlier in the week. Risk-sensitive currencies took some of the hardest hits, with AUD/USD briefly breaking below the 0.7000 handle, while USD/JPY pushed higher as the yen weakened against a broadly stronger greenback.

What makes this episode notable isn't just the data itself, but the political backdrop around it. President Trump, who handpicked Warsh specifically because he wanted lower rates after repeatedly clashing with Powell, responded to Wednesday's hawkish tilt with uncharacteristic restraint, telling reporters in Paris the decision was "all right, whatever" and that he's "guided by what" Warsh wants. Whether that patience holds if the committee actually moves toward a hike later this year is very much an open question, and probably the one Fed watchers will be asking most closely heading into the next meeting.

Want to stay ahead of major macro events? Follow us for daily market insights, breaking news, and analysis you can actually use.

Want to stay ahead of major macro developments that move the Forex market?

👉Follow Followme and check out the Weekly Economic Calendar

Download Followme Application

Follow us on:

免責事項:本記事で述べられている見解は著者の見解のみであり、Followmeの公式見解を反映するものではありません。Followmeは、提供された情報の正確性、完全性、信頼性について一切責任を負いません。また、書面で明示的に記載されている場合を除き、本記事の内容に基づいて行われたいかなる行動についても責任を負いません。

この記事が気に入ったら、著者にチップを送って感謝の気持ちを表しましょう。

-終わり-